Try Tidyflow

Get your firm organized.

Watch a 4-minute demo, or start a free trial. No credit card required.

Every software vendor, conference speaker, and industry publication is talking about AI in accounting. Most of it is hype. This guide cuts through the noise and covers what small accounting firms can actually use AI for today, what’s not ready yet, and how to get started without overhauling your entire workflow.

What AI Can Do For Your Firm Right Now

1. Draft Client Communication

AI is excellent at drafting routine emails, letters, and client updates. Instead of writing from scratch every time:

Use AI to draft:

- Fee increase letters

- Engagement letter templates

- Client onboarding emails

- Document request messages

- Year-end summary letters

- Deadline reminder emails

How: Paste your key details into ChatGPT, Claude, or a similar tool and ask it to draft the message in your firm’s tone. Review, adjust, and send. This turns a 15-minute writing task into 3 minutes.

Example prompt: “Draft a professional email to a client explaining that their monthly bookkeeping fee is increasing from $500 to $600 per month, effective July 1. The reason is that their transaction volume has increased from 80 to 150 per month. Tone: professional but friendly.”

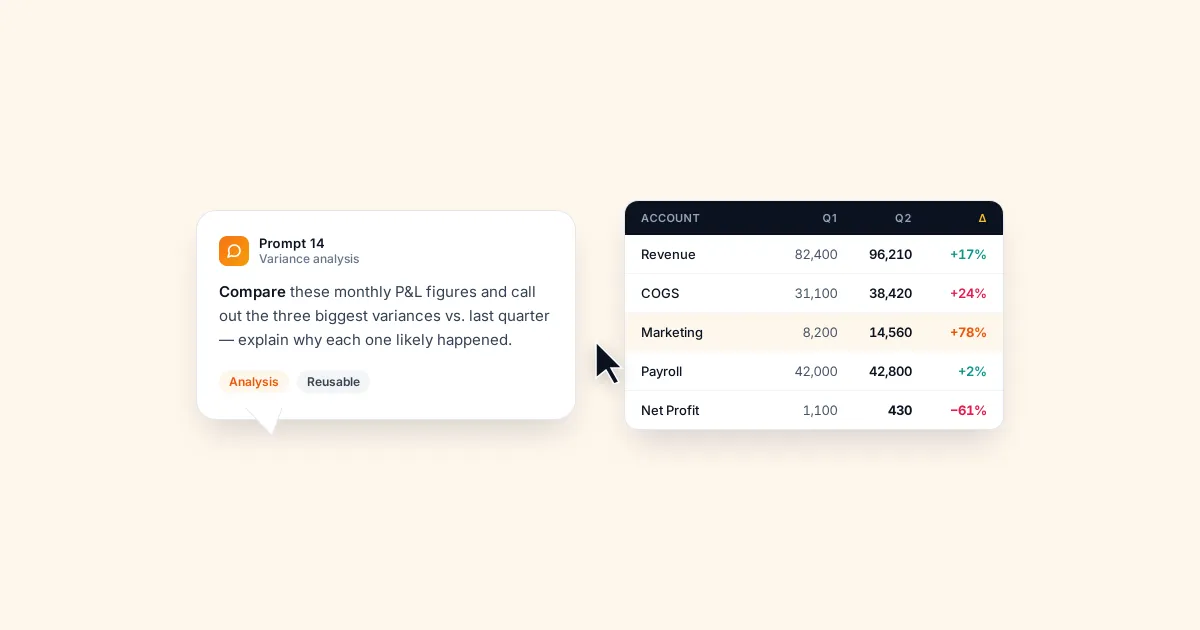

2. Summarize and Explain Financial Data

AI can take raw financial data and turn it into plain-English explanations for clients.

Use cases:

- Generate a narrative summary of monthly P&L results (“Revenue increased 12% month-over-month driven by a large project in the second week…”)

- Explain tax return outcomes in client-friendly language

- Create talking points for quarterly advisory meetings

- Summarize the implications of regulatory changes for specific client types

Important: Always review AI-generated financial summaries for accuracy. AI can hallucinate numbers or misinterpret context. Use it as a first draft, not a final product.

3. Speed Up Research

Tax law, regulatory requirements, and compliance deadlines change constantly. AI can help you research faster:

- “What are the current rules for instant asset write-off in Australia for the 2025-26 financial year?”

- “Summarize the key changes in the 2025 Tax Cuts and Jobs Act extension”

- “What deductions can a dentist typically claim as business expenses?”

Caveat: AI’s knowledge has a cutoff date and can be wrong about specific tax law details. Always verify against official sources (ATO, IRS, legislation) before advising clients. Use AI as a research accelerator, not an authority.

4. Create Standard Operating Procedures

AI is excellent at turning rough notes into structured SOPs:

Prompt: “I’m going to describe our monthly bookkeeping process. Turn it into a step-by-step SOP with clear action items. Here’s how we do it: [describe your process in bullet points]”

The AI will structure your notes into a clean, numbered procedure that you can refine and add to your process documentation.

5. Generate Content for Marketing

Blog posts, LinkedIn updates, email newsletters, and website copy — AI can help produce content at scale:

- Draft blog post outlines on accounting topics

- Generate LinkedIn post ideas based on your expertise

- Create email newsletter content for client updates

- Write meta descriptions and SEO titles for web pages

Quality note: AI-generated content needs significant editing to be valuable. The best approach is to have AI create a first draft, then rewrite it with your expertise, voice, and specific examples. Generic AI content without human editing is easy to spot and doesn’t build trust.

What AI Can’t Do Well (Yet)

Make Professional Judgement Calls

AI can tell you the rules. It can’t tell you how to apply them to your specific client’s situation. Tax planning, entity structuring, and financial strategy require professional judgement that AI doesn’t have.

Replace Client Relationships

Clients hire accountants they trust. Trust is built through personal interaction, understanding their business, and being there when they need advice. AI can’t replace that relationship — it can only free up time so you have more of it to invest in clients.

Guarantee Accuracy on Tax Law

AI models are trained on data with a cutoff date. Tax law changes constantly. AI can be confidently wrong about specific deductions, thresholds, and deadlines. Always verify.

Handle Sensitive Data Safely (By Default)

If you paste client financial data into ChatGPT, that data may be used for model training (depending on your settings and plan). Use business/enterprise plans with data privacy guarantees, or avoid pasting identifiable client information into AI tools.

Tools Worth Trying

General AI Assistants

| Tool | Best For | Cost |

|---|---|---|

| ChatGPT (OpenAI) | Drafting, research, brainstorming | Free–$20/month |

| Claude (Anthropic) | Long documents, analysis, nuanced writing | Free–$20/month |

| Microsoft Copilot | Firms using Microsoft 365 | Included in some M365 plans |

Accounting-Specific AI

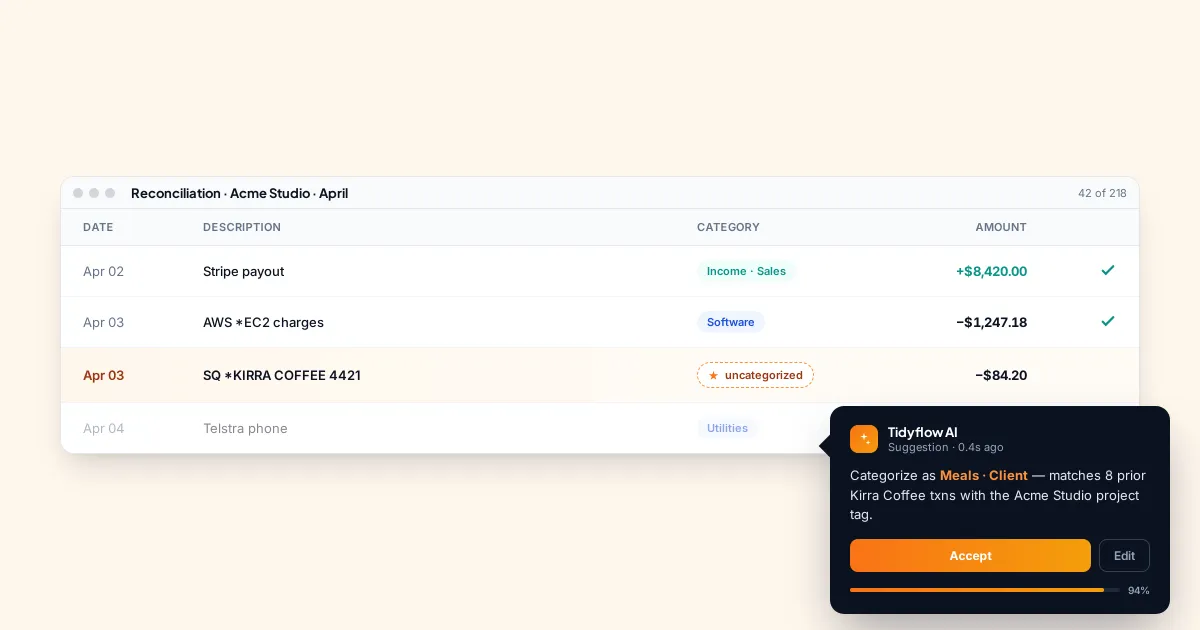

Some accounting software is building AI features directly into their platforms:

- Xero — AI-powered bank reconciliation suggestions

- QuickBooks — AI-assisted categorization and insights

- Various practice management tools — AI-generated client summaries and workflow suggestions

These are generally more useful than standalone AI tools because they work within your existing data and workflow.

Document Processing

AI-powered OCR and data extraction tools can read receipts, invoices, and bank statements:

- Dext (formerly Receipt Bank) — AI-powered receipt and invoice processing

- Hubdoc — Document collection and extraction

- AutoEntry — Automated data entry from documents

These tools save hours of manual data entry per week and are one of the most immediately impactful AI applications for accounting firms.

Getting Started With AI

Step 1: Start With One Use Case

Don’t try to “implement AI across your firm.” Pick one task where AI can save you time:

Best starting points:

- Drafting client emails (low risk, immediate time savings)

- Research questions (regulatory lookups, deduction lists)

- Creating SOP first drafts from your notes

Step 2: Create a Few Prompt Templates

Once you find prompts that work well, save them:

- “Draft a [type of email] to a client about [topic]. Tone: [professional/friendly/formal]. Include: [key points].”

- “Summarize this P&L data for a non-financial client. Highlight: revenue trend, major expenses, cash position. Keep it under 200 words.”

- “List the common tax deductions for [industry] in [country] for the [year] financial year.”

Step 3: Set Data Handling Rules

Before your team starts using AI, establish rules:

- Never paste client-identifiable information (names, TFN/SSN, bank accounts) into free AI tools

- Use business plans with data privacy guarantees if you’re processing client data

- Always review AI output before sending to clients or using in professional work

- Disclose when appropriate — some clients may want to know if AI was used in preparing their work

Step 4: Measure the Impact

Track how much time AI saves on the tasks you’ve adopted it for. If drafting client emails now takes 3 minutes instead of 15, that’s 12 minutes saved per email × 10 emails/week = 2 hours/week. That’s tangible and justifies further adoption.

The Realistic AI Timeline for Small Firms

Available now: Email drafting, research acceleration, content creation, document OCR, bank transaction categorization.

Coming soon (1–2 years): More sophisticated automated bookkeeping, AI-assisted tax return review, predictive cash flow analysis.

Further out (3–5 years): AI handling routine compliance work end-to-end with human oversight, automated advisory insights from client data.

The firms that will benefit most from AI in the future are the ones building familiarity with it now — not through massive investments, but through consistent, practical use in daily work.

The Bottom Line

AI isn’t going to replace accountants. It’s going to replace accountants who spend all their time on tasks AI can do — freeing the good ones to focus on advisory, client relationships, and strategic work that AI can’t touch.

Start small. Use AI for one repetitive task this week. See how much time it saves. Expand from there.

The firms that integrate AI thoughtfully into their workflow will be more efficient, more profitable, and better positioned for the future. The firms that ignore it will slowly fall behind — not because AI replaces them, but because competing firms will simply be faster and more productive.