Try Tidyflow

Get your firm organized.

Watch a 4-minute demo, or start a free trial. No credit card required.

Starting an accounting firm is one of the most reliable paths to building a profitable small business. The demand is constant, the margins are healthy, and the startup costs are low compared to most businesses. But knowing how to do accounting and knowing how to run a firm are different skills.

This guide covers everything from the initial decision through to getting your first clients and building systems that scale.

Step 1: Decide What Kind of Firm You’re Starting

Before anything else, clarify what you’re building:

Solo Practice

You do all the work yourself, possibly with an admin assistant or contractor as you grow.

- Startup cost: $2,000–10,000

- Revenue potential: $80,000–200,000/year (solo)

- Best for: Experienced accountants who want flexibility and low overhead

Small Firm (2–10 People)

You hire staff to do production work while you manage the firm, develop business, and handle complex work.

- Startup cost: $10,000–50,000

- Revenue potential: $300,000–1,500,000/year

- Best for: Accountants with management skills who want to build a team

Virtual / Remote Firm

No physical office. Team and clients are remote. Lower overhead, wider talent pool, broader client geography.

- Startup cost: $2,000–15,000

- Revenue potential: Same as above but with lower overhead

- Best for: Tech-savvy accountants comfortable working remotely

Most people start as a solo practice and grow into a small firm over 2–5 years. That’s the path this guide assumes.

Step 2: Handle the Legal Setup

Choose Your Business Structure

| Structure | Liability Protection | Tax Treatment | Complexity |

|---|---|---|---|

| Sole proprietorship | None | Personal | Simplest |

| LLC / LLP | Yes | Pass-through (flexible) | Moderate |

| S-Corp | Yes | Pass-through + payroll tax savings | More complex |

| Corporation | Yes | Double taxation (unless S-election) | Most complex |

Most common choice: LLC or LLP for new firms. Provides liability protection with flexible tax treatment. Consult your own accountant (yes, accountants need accountants) for the best structure given your situation.

Other Legal Requirements

- Register your business name (check availability in your state/country)

- Get an EIN / ABN / business tax number

- Open a business bank account (separate from personal)

- Get professional liability (E&O) insurance — $500–2,000/year for a solo practice

- Check CPA licensing requirements in your state (if applicable)

- Register with your state board of accountancy

- Set up a business address (home office or virtual office is fine)

Step 3: Define Your Services and Pricing

Don’t try to offer everything. Start with 2–3 core services you can deliver well:

Common Starting Points

Bookkeeping + Tax — monthly bookkeeping and annual tax preparation. The bread and butter of most small firms.

Tax Only — individual and small business tax preparation. Lower monthly revenue but simpler operations.

Bookkeeping + Advisory — monthly bookkeeping with financial review and advice. Higher value, higher price.

Set Your Prices Early

Don’t figure out pricing later. Set it before you get your first client.

Quick pricing framework:

- Decide your target annual income (e.g., $150,000)

- Add overhead costs (software, insurance, marketing — roughly $15,000–30,000/year for a solo practice)

- Divide by the number of billable hours you can realistically work (1,400–1,600/year for a solo practitioner)

- That’s your minimum effective hourly rate

Example: ($150,000 + $25,000) ÷ 1,500 hours = $117/hour minimum.

Now package your services at fixed fees that exceed that minimum. A bookkeeping client taking 5 hours/month should be priced at $600+ per month — not $400.

For detailed pricing guidance and example packages, see our guide on pricing accounting services.

Step 4: Set Up Your Tech Stack

The right tools from day one prevent painful migrations later.

Essential Software

| Category | Recommended Options | Cost |

|---|---|---|

| Accounting software | QuickBooks Online, Xero | $30–80/month |

| Practice management | Tidyflow, Karbon, Canopy | $39–80/user/month |

| Tax preparation | Drake, UltraTax, Lacerte | $1,000–4,000/year |

| Document management | Built into practice management, or Google Drive/Dropbox | Free–$15/user/month |

| E-signatures | Built into Tidyflow, or DocuSign, PandaDoc | Free–$25/month |

| Communication | Email + client portal (Tidyflow includes this) | Varies |

| Password manager | 1Password, Bitwarden | Free–$8/user/month |

| Video meetings | Zoom, Google Meet | Free–$15/month |

Total monthly cost for a solo practice: $165–400/month

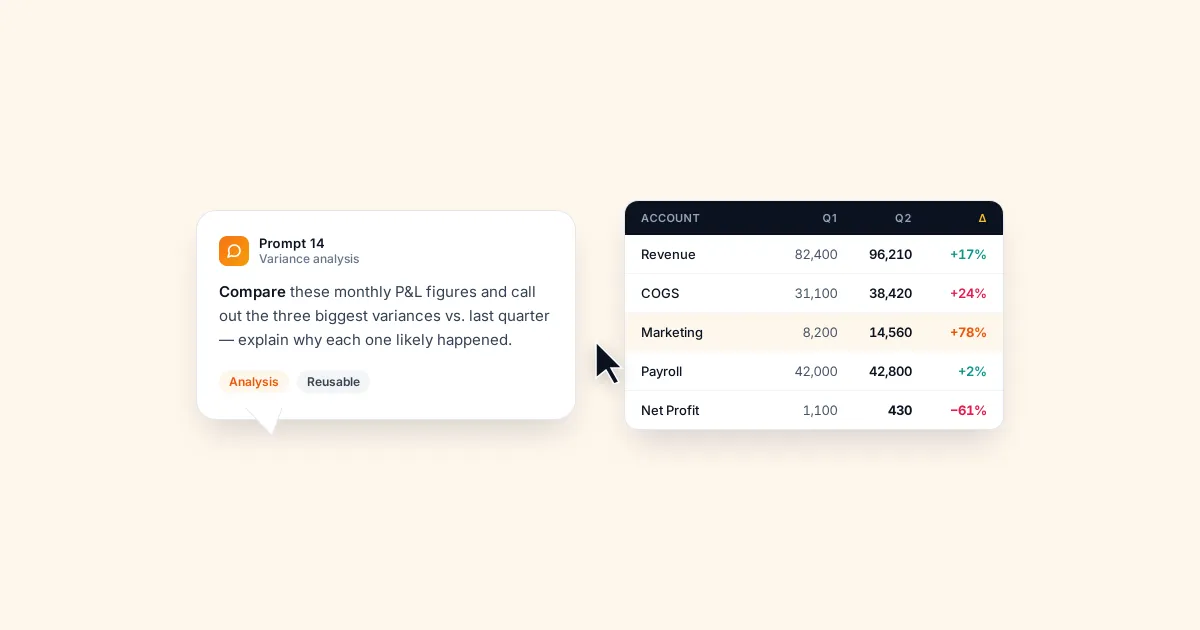

Why Practice Management Software Matters Early

A spreadsheet works for 5 clients. It breaks at 15. By 25 clients, you’re drowning in sticky notes and email threads, forgetting deadlines and losing track of what’s been done.

Practice management software like Tidyflow gives you:

- Job management — track every job across all clients with statuses and deadlines

- Client portal — clients upload documents and respond to requests in one place

- Recurring job templates — set up monthly bookkeeping, quarterly BAS, annual tax as templates. Apply them to new clients in seconds.

- Invoicing — send invoices and collect payments directly

- Client requests — request documents with automated reminders until clients respond

Starting with the right system means your 50th client is no harder to manage than your 5th. Tidyflow’s Core plan starts at $39/user/month ($29/user/month billed annually) — less than the cost of one hour of your time.

Step 5: Get Your First Clients

Your First 10 Clients (The Hardest Part)

The first 10 clients usually come from your personal network, not marketing:

- Tell everyone you know. Friends, family, former colleagues, LinkedIn connections. “I’ve started an accounting firm specializing in [niche]. If you know anyone who needs help with their books or taxes, I’d appreciate the introduction.”

- Tap your existing network. If you’re leaving a firm, some clients may follow you (check your employment agreement for non-compete clauses first).

- Offer a “founding client” rate. A modest discount for your first 5–10 clients in exchange for referrals and testimonials once you’ve delivered results.

- Contact local small business groups. Chambers of commerce, BNI groups, local Facebook groups for business owners.

From 10 to 50 Clients (Systematic Marketing)

Once you have a base of clients and some testimonials, shift to systematic lead generation:

- Google Business Profile — set up and optimize your listing. Ask happy clients for Google reviews. This is the highest-ROI marketing activity for local firms.

- Website with clear positioning — who you serve, what services you offer, pricing (or at least price ranges), and a clear call to action.

- Content marketing — write 1–2 blog posts per month targeting searches your ideal clients make (“bookkeeping for construction companies,” “how much does a small business accountant cost”).

- Referral partnerships — build relationships with financial advisors, business coaches, lawyers, and mortgage brokers who can refer clients to you.

For more detail on marketing strategies, see our guide on marketing for accounting firms.

Step 6: Build Systems That Scale

The firms that grow successfully are the ones that systematize early. Without systems, growth means more chaos. With systems, growth means more revenue without proportionally more stress.

Standardize Your Processes

For each service you offer, document:

- What information you need from the client before starting

- What steps are involved in completing the work

- What the deliverable looks like

- What the review/quality check process is

Turn these into job templates in your practice management software. Every new client of the same type gets the same template — ensuring nothing is missed and new team members can follow the process immediately.

Onboard Every Client the Same Way

Create a repeatable onboarding process:

- Engagement letter signed

- Intake form completed

- Portal access set up

- Accounting software connected

- Recurring jobs created

- Welcome email sent

See our client onboarding checklist for a detailed template.

Track Your Numbers

Monitor these monthly:

- Revenue per client — are you charging enough?

- Capacity utilization — are you near your limit or have room to grow?

- Client acquisition cost — what does it cost to win a new client?

- Client retention rate — what percentage renew or stay?

- Effective hourly rate — revenue ÷ hours worked. Should be above your minimum target.

Step 7: Plan for Growth

When to Hire Your First Person

Hire when you’re consistently turning away work or when your hours are unsustainable (50+ hours/week for more than 3 months). Not before.

First hire options:

- Bookkeeper or junior accountant — take over production work so you can focus on client relationships, business development, and complex work

- Virtual assistant / admin — handle scheduling, email, and administrative tasks

- Contractor / freelancer — seasonal help for tax season without the commitment of a full-time hire

Typical Growth Timeline

| Milestone | Timeline | Revenue (Approx.) |

|---|---|---|

| First client | Month 1–3 | — |

| 10 clients | Month 3–9 | $60,000–120,000/year |

| First hire | Year 1–2 | $150,000–250,000/year |

| 30+ clients | Year 2–3 | $250,000–500,000/year |

| Team of 3–5 | Year 3–5 | $500,000–1,000,000/year |

These are rough benchmarks — your timeline will depend on your niche, pricing, and how aggressively you pursue growth.

Common Mistakes

Underpricing. New firm owners often price low to win clients. This creates a race to the bottom and attracts price-sensitive clients who are the hardest to serve. Charge what you’re worth from day one.

Not choosing a niche. “I serve small businesses” is not a positioning. Pick a niche and own it. You’ll get better referrals, charge higher prices, and market more effectively.

Buying too much software too early. Start lean. You need accounting software, practice management, and a tax tool. Everything else can wait.

Waiting for perfection. Your website doesn’t need to be perfect. Your processes don’t need to be perfect. Your first client doesn’t need a flawless experience. Start, learn, improve.

Not separating personal and business finances. Open a business bank account on day one. Commingling funds is an accounting sin and a legal risk.

Startup Cost Summary

| Item | One-Time Cost | Monthly Cost |

|---|---|---|

| Business registration | $100–500 | — |

| Professional liability insurance | — | $50–150 |

| Website (basic) | $500–2,000 | $20–50/month hosting |

| Accounting software | — | $30–80 |

| Practice management (Tidyflow) | — | $29–69/user |

| Tax software | $1,000–4,000/year | — |

| Marketing (initial) | $500–2,000 | $100–500 |

| Office / equipment | $500–3,000 | — |

| Total | $2,600–11,500 | $229–849/month |

You can start a viable accounting firm for under $5,000 total if you work from home, use affordable software, and do your own marketing. That’s one of the lowest startup costs of any professional services business.

Start This Week

- Decide your structure (solo/firm) and niche

- Register your business and get insurance

- Set up your tech stack (accounting software + Tidyflow + tax software)

- Define your services and pricing

- Tell everyone you know that you’ve started

- Land your first client

The barrier to starting an accounting firm has never been lower. The tools are affordable, the work can be done remotely, and the demand for good accountants far exceeds the supply. The hardest part isn’t starting — it’s deciding to do it.